How I Stopped Putting All My Eggs in One Basket — A Real Talk on Global Diversification

For years, I thought investing meant just picking stocks in my home market. Then came the market dip that wiped out months of gains — a wake-up call. That’s when I started exploring overseas assets, not for hype, but for real protection. Diversifying across borders wasn’t easy at first, but it changed how I see risk and growth. This is my journey — the mistakes, the lessons, and the strategy that finally made my portfolio resilient. What began as a reaction to loss evolved into a disciplined approach: one that balances opportunity with caution, familiarity with exploration, and short-term discomfort with long-term security. This is not a story of overnight success, but of gradual learning — and it’s one that could reshape how you think about your own financial future.

The Wake-Up Call: When Home Market Risk Hits Hard

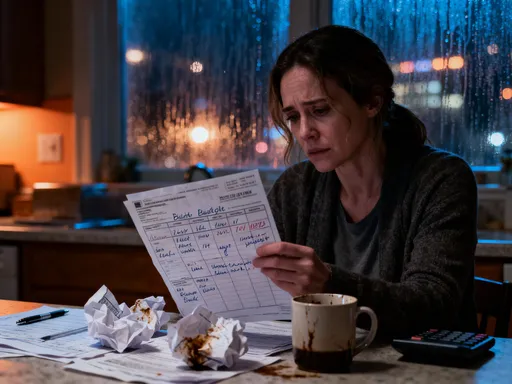

It started with a single quarter — three months that erased nearly 18% of my portfolio’s value. I hadn’t done anything reckless. I held a mix of blue-chip stocks and dividend-paying companies, all within my home country. These were names I trusted, industries I understood, and performance I’d watched for years. But when inflation spiked, interest rates climbed, and consumer spending slowed, the entire domestic market reacted in unison. My investments, once steady, began to slide — not because of individual company failures, but because the whole economic ecosystem was under pressure.

That’s when it hit me: I had never truly diversified. All my assets were tied to one economy, one currency, and one regulatory environment. I was relying entirely on the health of a single financial system. Asset concentration, I realized, wasn’t just a technical term — it was a silent risk I’d ignored. Most investors assume diversification means owning different stocks. But if all those stocks operate in the same country and respond to the same economic forces, true diversification doesn’t exist. The domino effect was clear: one national crisis triggered losses across every holding, regardless of sector or size.

Emotional attachment played a big role, too. I felt more comfortable investing in companies I could visit, whose products I used, and whose news I read daily. This familiarity gave me a false sense of control. Behavioral finance calls this the “home bias” — the tendency to favor domestic investments simply because they feel safer. But feeling safe isn’t the same as being safe. When the downturn came, I watched helplessly as my portfolio dropped in tandem with the national index. There was no cushion, no offsetting gains from elsewhere. It was a painful lesson: putting all your eggs in one basket, even a well-known one, leaves you exposed when the ground shakes.

Why Go Global? Beyond the Hype of Overseas Investing

After that setback, I began researching global diversification not as a trend, but as a necessity. I discovered that economies don’t move in lockstep. While my home market struggled with inflation, other regions were stabilizing. Some emerging markets were growing rapidly due to infrastructure investment and young populations. Developed economies in different time zones were recovering from earlier cycles. This realization shifted my perspective: geography isn’t just a detail — it’s a strategic advantage.

The core benefit of international exposure lies in decoupling risk. Different countries experience economic booms and recessions at different times. For example, when one nation tightens monetary policy, another may be loosening it to stimulate growth. These divergent cycles mean that while your domestic assets might be under pressure, your overseas holdings could be gaining momentum. Over time, this balance smooths out volatility and improves risk-adjusted returns. It’s not about chasing higher returns abroad — it’s about reducing the impact of local downturns.

Currency diversification adds another layer of protection. Holding assets in multiple currencies means you’re not fully exposed to the depreciation of your home currency. If your local money loses value due to inflation or trade imbalances, foreign-denominated investments can help preserve purchasing power. This doesn’t mean betting on currency movements — that’s speculation. Instead, it’s about natural hedging: owning real assets abroad that generate income in different monetary systems.

Access to innovation is another overlooked benefit. Some of the most transformative industries — from renewable energy in Scandinavia to fintech in Southeast Asia — are growing outside traditional financial centers. By staying local, investors miss early exposure to these trends. Global diversification isn’t about abandoning homegrown success — it’s about expanding your opportunity set. Think of it like weather patterns: storms rarely blanket the entire planet at once. Just as farmers in one region suffer drought while others enjoy rain, economies operate on different rhythms. Smart investors learn to plant seeds in multiple climates.

Breaking Down Barriers: What Stops People from Going Abroad

If global diversification is so beneficial, why do so many investors hesitate? In my early research, I found that the obstacles weren’t always financial — they were psychological and practical. The biggest barrier was confusion. Foreign tax rules, withholding taxes on dividends, reporting requirements — the terminology alone felt overwhelming. I worried about making a mistake that could trigger penalties or unexpected costs. Many platforms didn’t clearly explain how cross-border investing worked, leaving me to piece together information from forums and outdated guides.

Fees were another concern. I’d heard stories of high transaction costs, currency conversion charges, and hidden custodial fees. While some of these are real, I learned that many low-cost, regulated platforms now offer transparent pricing for international access. The key is due diligence: comparing fee structures, understanding settlement times, and confirming regulatory oversight. What once seemed like a minefield became manageable with the right tools and information.

Language and cultural differences also created hesitation. I wasn’t fluent in other financial systems, and reading foreign market reports felt intimidating. But I realized I didn’t need to understand every detail. Just as I invest in multinational companies without knowing every factory location, I could rely on well-managed funds and trusted intermediaries to handle complexity. The goal wasn’t to become an expert in foreign markets — it was to gain exposure through reliable channels.

Perhaps the most subtle barrier was emotional comfort. There’s a deep-seated preference for the familiar. We trust what we know, and we fear what we don’t. This is reinforced by confirmation bias — the tendency to seek information that supports existing beliefs. News outlets focus on domestic markets, financial advisors often specialize locally, and social conversations revolve around familiar companies. All of this creates a feedback loop that makes global investing feel risky, even when data shows otherwise. Recognizing this bias was crucial. I had to accept that discomfort is part of growth — and that avoiding it could cost me more in the long run.

Building the Foundation: How to Start Diversifying Without Overcomplicating

My first step wasn’t to open accounts in five countries or buy foreign real estate. I started small, focusing on simplicity and accessibility. The most effective entry point was globally diversified exchange-traded funds (ETFs). These funds hold a mix of international stocks and bonds, spanning developed and emerging markets. They’re traded like regular stocks, require no direct interaction with foreign brokers, and offer instant diversification. I chose funds with low expense ratios, clear holdings, and a track record of consistent performance.

Another strategy was investing in multinational companies listed on my home exchange. These are firms that generate significant revenue overseas — think global manufacturers, technology giants, or consumer brands with international reach. By owning their shares, I gained indirect exposure to foreign economies without dealing with cross-border transactions. This approach allowed me to maintain familiarity while expanding geographic reach. It wasn’t full diversification, but it was a meaningful first step.

I also explored digital investment platforms that offer seamless access to international markets. Many of these are regulated, user-friendly, and designed for retail investors. I evaluated each platform based on security, transparency, customer support, and fee structure. I looked for features like automated currency conversion, tax reporting assistance, and educational resources. The goal was to reduce friction, not add complexity. I started with a small allocation — just 10% of my portfolio — to test the process and build confidence.

Diligence was essential. I reviewed the custodian’s regulatory status, checked for investor protection schemes, and confirmed how assets were held. I also paid attention to liquidity — ensuring I could exit positions without excessive delays or costs. Starting with indirect exposure through funds and multinationals gave me time to learn. I avoided chasing high-growth but volatile emerging markets early on. Instead, I prioritized stability, transparency, and ease of management. This foundation allowed me to scale gradually, adding direct international holdings only after gaining experience.

Balancing Act: Mixing Local and Global for True Resilience

Diversification isn’t about rejecting home — it’s about balance. I didn’t sell all my domestic holdings. Instead, I restructured my portfolio to reflect a more resilient mix. My core remained in high-quality local assets: companies with strong balance sheets, reliable dividends, and long-term growth potential. But I now allocate a growing portion — currently around 35% — to international investments. This split isn’t arbitrary; it’s based on economic fundamentals, not trends or emotions.

Geographic allocation required research. I looked at GDP growth forecasts, inflation trends, political stability, and demographic shifts. I didn’t chase the hottest market of the year. Instead, I focused on regions with sustainable economic models — places where innovation, education, and infrastructure support long-term development. For example, I increased exposure to certain Asian economies with rising middle classes and strong export sectors, while maintaining steady positions in European markets known for regulatory stability and corporate governance.

Rebalancing became a regular practice. Every six months, I reviewed my portfolio’s performance and adjusted allocations to stay aligned with my targets. If one region outperformed, it might grow to represent a larger share than intended. I’d then sell a portion to rebalance, locking in gains and maintaining discipline. This process prevented emotional decisions — like holding onto a winning asset too long or panic-selling after a dip.

Currency fluctuations added another dimension. I learned to view them not as distractions, but as part of the global investing reality. A stronger foreign currency could boost returns when converted back home, while a weaker one could temporarily reduce them. But over time, these swings tend to average out. I avoided trying to time currency movements — that’s speculation, not strategy. Instead, I focused on owning real assets in diverse economies, confident that long-term value would prevail over short-term volatility. Patience, I discovered, was more valuable than perfect timing.

Risk Control: Protecting Gains Without Killing Growth

Global diversification reduces risk, but it doesn’t eliminate it. Markets everywhere can fall. Geopolitical tensions, regulatory changes, or global recessions can affect multiple regions at once. That’s why I built additional safeguards into my strategy. One key tool was the use of stop-loss orders — automatic instructions to sell a holding if it drops below a certain price. This helped limit downside risk without requiring constant monitoring. I set these levels based on historical volatility and long-term outlook, not short-term noise.

I also addressed currency risk more directly. While some fluctuation is natural, extreme movements can erode gains. To mitigate this, I explored currency-hedged funds — investment vehicles that reduce exposure to exchange rate swings. These aren’t always necessary, but they can be useful during periods of high currency volatility. I didn’t hedge everything — that would negate one of diversification’s benefits — but I used selective hedging to protect core holdings during uncertain times.

Asset class diversification complemented my geographic strategy. I spread investments across equities, bonds, and real estate in different regions. When stock markets dipped, bond holdings often provided stability. Real estate investment trusts (REITs) in growing urban centers offered income and inflation protection. This multi-layered approach ensured that no single market or asset type dominated my portfolio’s fate.

Monitoring became an ongoing habit. I tracked macroeconomic indicators — interest rate decisions, employment data, trade balances — not to predict the future, but to stay informed. I paid attention to geopolitical developments, not out of fear, but to understand potential risks. When I misjudged a market — such as underestimating regulatory changes in a certain country — I analyzed the mistake, adjusted my process, and moved forward. Risk control, I learned, isn’t about avoiding losses entirely — it’s about managing them with discipline and clarity.

The Long Game: Why Diversification Pays Off Over Time

The real value of global diversification didn’t show up in quarterly statements — it showed up in peace of mind. During the next market downturn, I didn’t panic. I watched my domestic holdings dip, but saw my international assets holding steady or even gaining. The overall portfolio decline was smaller, and recovery came faster. I avoided the emotional trap of selling low, simply because I wasn’t fully exposed to one collapsing market.

Over five years, the compound effect became clear. While no single investment delivered overnight riches, the combined performance of a balanced, globally diversified portfolio produced steadier growth. Volatility was lower, drawdowns were shallower, and compounding worked more efficiently because there were fewer large setbacks to recover from. The financial return was meaningful, but the psychological return was even greater: confidence.

I no longer view investing as a gamble on one economy’s fate. I see it as a long-term strategy of resilience — building a financial foundation that can withstand storms, adapt to change, and continue growing. Diversification isn’t a guarantee of profits, but it is a proven way to manage risk. It won’t make you rich overnight, but it can help you stay wealthy over time. For anyone serious about lasting financial health, it’s not an option — it’s a responsibility. The world is interconnected, and your portfolio should reflect that reality. By spreading your investments across borders, you’re not running from risk — you’re managing it wisely, one thoughtful decision at a time.