Why Passive Income Dreams Can Backfire — A Reality Check

You’ve probably heard that passive income is the golden ticket to financial freedom. Many believe it offers a way to earn money without trading time for dollars, promising flexibility, early retirement, and peace of mind. I believed it too—until I lost money, wasted time, and hit unexpected roadblocks. The truth? Not all passive income streams are created equal, and market shifts can turn your side hustle into a financial headache. Behind the glossy social media posts and viral success stories lies a more complicated reality. This is a real talk about what most guides won’t tell you: the hidden pitfalls, the overhyped trends, and how to analyze opportunities like a pro. Because while passive income can be powerful, it’s not a magic formula—and treating it as such can cost you more than just money.

The Allure of Passive Income: Why Everyone’s Chasing It

The dream of passive income has never been more popular. It speaks directly to a deep desire for control—control over time, over location, over one’s financial future. In an era of rising living costs and uncertain job markets, the idea of building income that works for you, even while you sleep, is deeply appealing. People imagine waking up to notifications of earnings from rental properties, dividend payouts, or digital products selling automatically online. The cultural narrative is clear: if you’re not building passive income, you’re falling behind.

This movement has been fueled by the rise of digital platforms and social media, where influencers share stories of earning thousands per month from minimal effort. Blogs, podcasts, and YouTube channels are filled with tales of people quitting their jobs after launching an eBook, creating an online course, or investing in real estate. These stories are compelling, often presented with clean visuals, bank statements, and lifestyle shots from tropical locations. But what these narratives rarely show is the years of trial and error, the failed launches, or the hidden responsibilities behind the scenes. The allure is real, but so is the risk of being misled by selective storytelling.

Moreover, economic conditions have amplified the appeal. With inflation eroding savings and traditional pensions becoming rare, individuals feel increasing pressure to take charge of their financial security. The gig economy has normalized side hustles, and many now view multiple income streams as essential, not optional. Passive income, in particular, promises a way to break free from the linear relationship between time and money. However, this widespread enthusiasm often overlooks a critical truth: passive income is not passive in the way most people assume. It requires strategy, capital, and ongoing attention—elements that are rarely emphasized in the success stories that dominate the conversation.

What Passive Income Really Means (And What It Doesn’t)

At its core, passive income refers to money earned with minimal ongoing effort after the initial setup. But the word “minimal” is where most misconceptions begin. True passive income—where revenue flows with almost no involvement—is rare. More commonly, what people call passive income is actually semi-passive, requiring regular maintenance, updates, oversight, or reinvestment. For example, owning rental property may generate monthly income, but it also demands tenant management, repairs, insurance, and tax compliance. A dividend-paying stock portfolio may deliver quarterly payouts, but it still requires research, rebalancing, and monitoring of market conditions.

The confusion often starts with language. Calling something “passive” makes it sound effortless, which can lead individuals to underestimate the work involved. This mislabeling can result in poor planning, inadequate preparation, and eventual frustration when the reality sets in. Consider digital products like eBooks or online courses. While they can sell repeatedly without additional labor per transaction, they still require marketing, customer support, platform maintenance, and periodic content updates to stay relevant. If neglected, sales decline, and the income stream dries up. In this sense, the income is scalable, but not truly passive.

Understanding the spectrum of effort is crucial. On one end are high-effort, active income models like consulting or freelancing. On the other end are truly low-touch models like certain royalty streams or well-managed index fund dividends. Most opportunities fall somewhere in the middle. The key is to evaluate each opportunity based on its actual time and resource requirements, not its marketing label. By doing so, individuals can set realistic expectations and avoid the disappointment that comes from assuming a venture will run itself. Recognizing that effort doesn’t disappear—it’s front-loaded or spread out—can lead to better decision-making and more sustainable outcomes.

Market Analysis: Why Timing and Trends Matter More Than You Think

Even the most well-structured passive income strategy can fail if it’s built on a shaky market foundation. Timing and trends play a decisive role in determining whether an opportunity thrives or collapses. For instance, entering the short-term rental market in 2018 might have seemed like a smart move, but by 2023, oversaturation, stricter regulations, and changing traveler behavior significantly reduced profit margins in many cities. Similarly, investing in certain tech stocks during the pandemic-driven surge led to strong returns initially, but a lack of attention to long-term fundamentals left many investors exposed when valuations corrected.

Real estate offers a clear example of how market cycles impact passive income. During boom periods, property values rise, rental demand increases, and financing is accessible. This creates an illusion of easy wealth. But in downturns, vacancies rise, maintenance costs eat into profits, and refinancing becomes difficult. Those who bought at peak prices without stress-testing their cash flow often found themselves in negative equity or forced to sell at a loss. The same principle applies to digital ventures. A niche website or app that thrives under one algorithm update may lose visibility overnight when platforms change their ranking criteria. Google’s frequent search algorithm updates have wiped out entire affiliate marketing businesses that relied on outdated SEO tactics.

Emerging trends also require careful evaluation. The rise of artificial intelligence, for example, has led to a surge in AI-powered tools and digital content creation. While some early adopters have found success, others have invested in platforms or services that quickly became obsolete as technology evolved. The key is not to chase trends blindly but to assess their sustainability. Questions to consider include: Is there lasting demand? Is the market overcrowded? Are regulatory risks emerging? By studying historical patterns and current indicators, investors can make more informed decisions and avoid entering markets at the wrong time. Passive income is not immune to economic forces—ignoring them is a recipe for financial setbacks.

The Hidden Costs No One Talks About

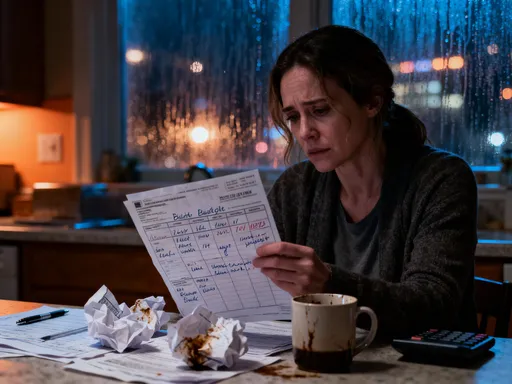

When evaluating passive income, most people focus on potential returns, but few account for the full range of hidden costs. These expenses—both financial and emotional—can significantly reduce net gains and increase the overall risk of a venture. One of the most overlooked is time. Even if an income stream requires only a few hours per month, those hours have value. Time spent managing tenants, updating a website, or reviewing investment performance could be used for family, rest, or other pursuits. This opportunity cost is real, even if it doesn’t appear on a balance sheet.

Financially, passive income often comes with ongoing expenses that eat into profits. Rental properties incur property taxes, insurance, maintenance, and management fees. Dividend stocks may generate income, but they are subject to capital gains taxes and may require advisory fees if managed through a financial professional. Digital products sold online face platform fees, payment processing charges, and potential costs for hosting, marketing, and customer service. In some cases, these expenses can consume 20% to 40% of gross income, turning what looks like a healthy return into a marginal one.

There’s also the emotional toll. Passive income ventures can create stress, especially when unexpected problems arise. A burst pipe in a rental unit at midnight, a sudden drop in ad revenue, or a negative review that goes viral can all trigger anxiety and sleepless nights. The belief that passive income leads to freedom can ironically lead to a new kind of pressure—the fear of losing what you’ve built. Additionally, many people underestimate the psychological burden of managing money they depend on. When passive income becomes a critical part of one’s budget, any disruption feels more urgent and stressful. Recognizing these hidden costs allows for more honest planning and helps individuals choose ventures that align with their true goals and lifestyle preferences.

Risk Control: Protecting Yourself Without Killing Your Returns

Passive income should not mean passive risk management. In fact, because many passive ventures operate in the background, they can lull investors into a false sense of security. A well-structured strategy includes built-in safeguards to protect capital while still allowing for growth. The first and most important principle is diversification. Relying on a single income stream—whether it’s one rental property, one online course, or one stock—creates vulnerability. If that stream fails, the entire financial plan is at risk. Spreading investments across different asset classes, industries, and geographies reduces exposure to any single point of failure.

Another essential tool is scenario planning. Before committing to any opportunity, it’s wise to ask: What if occupancy drops by 30%? What if interest rates rise? What if a competitor enters the market with a better product? Stress-testing a model under various conditions helps identify weaknesses and prepares the investor for downturns. For example, a rental property that barely breaks even at 90% occupancy may become a financial burden if the market shifts and vacancies rise. Building in a margin of safety—such as requiring a property to cash-flow positively even at 70% occupancy—can prevent future losses.

Equally important is having clear exit strategies. Knowing when to walk away is a sign of discipline, not failure. If a venture consistently underperforms, requires more time than expected, or no longer aligns with personal goals, it may be time to liquidate or shut it down. Holding on out of pride or hope can lead to greater losses. Additionally, setting performance benchmarks and reviewing them regularly ensures that passive income streams remain viable. Risk control isn’t about avoiding all risk—it’s about managing it intelligently so that setbacks don’t derail long-term financial health.

Smart Entry Points: How to Evaluate Opportunities Like a Pro

Not every passive income idea is worth pursuing. The key to success lies in disciplined evaluation before making any commitment. A professional approach involves asking a series of critical questions: Is there genuine, sustained demand for this product or service? Who is the competition, and what differentiates this offering? Can it scale without proportional increases in effort or cost? And perhaps most importantly, is it sustainable over time? These questions help separate fleeting trends from durable opportunities.

One effective framework is the “Four Pillars” method: assess demand, competition, scalability, and sustainability. Demand should be based on real data, not assumptions. Tools like Google Trends, industry reports, or customer surveys can provide insight into whether interest is growing, stable, or declining. Competition analysis reveals whether the market is oversaturated or if there’s room for a new player. Scalability determines whether the model can grow without requiring constant hands-on involvement. Sustainability considers external risks—regulatory changes, technological disruption, or economic shifts—that could undermine the business in the future.

Red flags include promises of high returns with little effort, lack of transparency about costs, or reliance on a single platform or partner. Green lights include recurring revenue models, low customer acquisition costs, and strong customer retention. For example, a subscription-based service with a loyal user base is generally more reliable than a one-time product with no repeat customers. By applying a structured evaluation process, individuals can avoid costly mistakes and focus on opportunities with the highest probability of long-term success. The goal is not to find the perfect idea, but to make informed choices that align with personal capacity and financial goals.

Building a Resilient Passive Income Strategy for the Long Game

Sustainable financial freedom is not achieved through quick wins or viral successes. It’s built through consistency, patience, and adaptability. A resilient passive income strategy combines the lessons of market awareness, cost management, risk control, and careful evaluation into a cohesive plan. Instead of chasing the next big thing, it focuses on steady progress, diversified income sources, and continuous learning. The most successful individuals don’t rely on a single stream—they build a portfolio of complementary assets that balance risk and reward.

This long-term approach begins with clear goals. Is the objective to supplement current income, achieve early retirement, or gain location independence? The answer shapes the strategy. It also requires realistic timelines. Most passive income models take 12 to 36 months to become profitable, and returns compound over time. Impatience often leads to poor decisions, such as cutting corners or abandoning a venture too soon. Discipline in tracking performance, reinvesting profits wisely, and adjusting to changing conditions is essential.

Finally, resilience means being prepared to evolve. Markets change, technologies advance, and personal circumstances shift. A strategy that works today may need adjustments tomorrow. The ability to pivot—whether by updating a digital product, refinancing a property, or reallocating investments—is what ensures longevity. Passive income, when approached with clarity and caution, can be a powerful tool for financial security. But it demands respect, preparation, and a willingness to look beyond the hype. The real reward isn’t just the money—it’s the peace of mind that comes from knowing your finances are built on a solid, thoughtful foundation.