How I Survived My Business Crash — Real Financial Planning That Works

What happens when your business suddenly fails and your income vanishes overnight? I’ve been there — drained accounts, mounting stress, and the terrifying silence of an empty bank balance. Instead of panicking, I rebuilt my finances from the ground up using practical planning strategies that actually work. This is not theory — it’s what saved me. If you’ve ever feared financial collapse, this story might be exactly what you need to hear. It’s a journey through shock, survival, and recovery — one that reveals the real tools of financial resilience. No magic formulas, no overnight fixes, just honest lessons learned from losing nearly everything and finding a way back.

The Day Everything Fell Apart

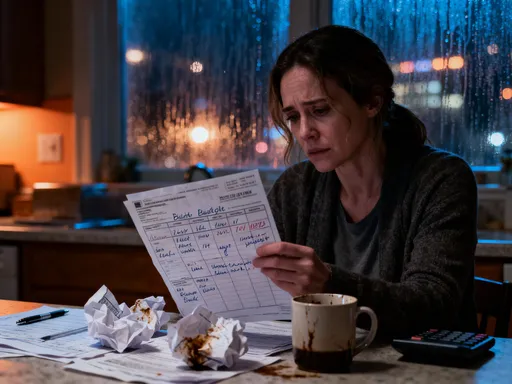

It started with a phone call from my accountant on a quiet Tuesday morning. The tone in her voice was different — hesitant, almost apologetic. She didn’t say the words outright, but I understood immediately: the business was insolvent. Our largest client had pulled out unexpectedly, and without that revenue, we couldn’t cover payroll, let alone rent or loan payments. Within 48 hours, the bank froze our operating account. Emails went unanswered. Suppliers stopped deliveries. The office, once buzzing with energy, became a hollow shell of silence.

That week, I sat at my kitchen table, staring at spreadsheets that no longer made sense. Numbers I had trusted for years now told a story of slow erosion — not sudden recklessness, but a series of small oversights that added up to disaster. I had assumed the business was stable because revenue was steady, but I hadn’t accounted for how fragile that stability really was. One contract loss, one economic dip, and the entire structure collapsed. The emotional toll was immediate. I felt shame, not just for the failure, but for the illusion of control I had maintained for so long.

What struck me most was how quickly everything changed. One day, I was managing a team, planning growth, and making decisions with confidence. The next, I was calculating how long my personal savings could last. Could I afford groceries? Could I pay the mortgage? The fear wasn’t just about money — it was about identity. For over a decade, my self-worth had been tied to the success of the business. When it failed, I felt like I had failed. But in that darkness, a small, stubborn voice emerged: survival was still possible. It wouldn’t come from luck or wishful thinking — it would come from strategy, discipline, and a complete rethinking of how I handled money.

Why Most Emergency Plans Fail When You Need Them Most

Before the crash, I believed I was prepared. I had an emergency fund — about three months of personal expenses tucked away in a savings account. I told myself that if anything went wrong, I’d be fine. But when the crisis hit, that fund disappeared in eight weeks. Why? Because I hadn’t planned for the full scope of a real emergency. Most people think of emergencies as short-term setbacks — a car repair, a medical bill, a few weeks of reduced income. But a business collapse is different. It’s not a bump in the road; it’s the road vanishing beneath you.

The flaw in most emergency planning is that it’s built on optimism, not reality. People assume they’ll find another job quickly, that expenses will stay the same, or that they can temporarily live off savings without making major changes. But in a true financial crisis, income doesn’t just dip — it stops. And expenses don’t freeze — they often increase. Legal fees, debt payments, and the cost of restructuring can add unexpected burdens. Meanwhile, emotional stress leads to poor decisions: selling assets too fast, taking on high-interest loans, or avoiding the problem altogether.

Another common mistake is confusing liquidity with readiness. Just because money is in a savings account doesn’t mean it’s structured for crisis use. Without clear rules for when and how to access it, people either hoard it out of fear or burn through it too quickly. I did both — I waited too long to use my savings, then spent recklessly once I started. The truth is, most emergency plans fail because they lack specificity. They don’t define what counts as an emergency, how much is needed, or what behaviors are allowed when the fund is active. A plan that works must be designed not just for numbers, but for human behavior under pressure.

Additionally, many people overlook the difference between personal and business emergencies. In a business failure, personal finances are directly impacted, but the solutions aren’t always the same. Using personal savings to cover business debts might feel like a fix, but it often drains resources needed for long-term survival. A robust plan must separate these domains and create clear boundaries. Without that separation, one failure can destroy both professional and personal stability. The lesson I learned is that preparation isn’t about having a fund — it’s about having the right kind of fund, with the right rules, at the right time.

Building a Realistic Financial Firewall

After the crash, I realized I needed more than an emergency fund — I needed a financial firewall. This isn’t a dramatic term; it’s a practical system designed to protect personal finances when business income disappears. A firewall isn’t about hoarding large sums of money. It’s about creating a structured buffer that prevents panic-driven decisions and buys time to think clearly. The goal isn’t wealth — it’s stability. And stability, I learned, comes from design, not luck.

A financial firewall has three core components: separation, structure, and triggers. First, personal and business finances must be completely separated. Before my business failed, I often moved money between accounts to cover gaps, blurring the lines between what was personal and what was operational. That made it easy to underestimate how much I was personally relying on business income. After the recovery, I established a strict rule: business revenue funds business expenses, and personal living costs are covered by a dedicated personal account. This separation creates clarity and prevents cross-contamination during a crisis.

The second component is structure. The firewall account isn’t a general savings fund — it has a specific purpose and clear rules. I set it to cover six months of essential personal expenses: housing, utilities, groceries, insurance, and basic transportation. It’s kept in a high-yield savings account, easily accessible but not linked to my daily spending. Most importantly, withdrawals are governed by a simple rule: only one withdrawal per month, and only for pre-defined essentials. This prevents impulsive spending and extends the fund’s lifespan.

The third element is triggers — clear signals that activate the firewall. These aren’t based on emotion, but on measurable thresholds. For example, if business revenue drops below 30% of average for two consecutive months, or if cash reserves fall below a certain level, the firewall engages automatically. This removes guesswork and delays. I also set up monthly financial check-ins to review these metrics, ensuring I’m not ignoring early warnings. A financial firewall doesn’t guarantee success, but it creates space to respond instead of react. It’s not a safety net — it’s a strategic buffer that turns crisis into a manageable challenge.

Cutting Costs Without Killing Your Future

When income stops, cutting expenses becomes unavoidable. But not all cost reductions are equal. The goal isn’t just to survive — it’s to preserve the ability to rebuild. I learned this the hard way. In the first months after the crash, I slashed everything: canceled subscriptions, sold my car, moved to a smaller apartment. While these moves helped, some decisions had long-term consequences. Selling my car saved money short-term, but it limited my ability to take on freelance work that required travel. I had cut too deeply, sacrificing future opportunities for immediate relief.

The key is to distinguish between survival costs and growth investments. Survival costs are non-negotiable — food, shelter, healthcare. Growth investments are expenses that maintain or enhance future earning potential, like internet access, professional development, or reliable transportation. These should be protected as long as possible. I created a two-tier budget: Tier One for survival, Tier Two for growth. When money was tight, I reduced Tier Two, but I didn’t eliminate it. For example, instead of canceling my internet, I switched to a lower-cost plan. Instead of quitting professional courses, I paused them temporarily.

Another effective strategy was renegotiation. I called every service provider — insurance, phone, utilities — and asked for lower rates or payment plans. Many agreed, especially when I explained the situation honestly. I also paused non-essential subscriptions and shifted to cash-only spending for discretionary items. This created a psychological barrier against impulse purchases. I set a weekly spending limit and used a prepaid card to enforce it. These small changes added up. Over three months, I reduced my monthly outflow by 38%, giving me nearly two extra months of runway.

The mindset shift was just as important as the tactics. I stopped viewing cost-cutting as punishment and started seeing it as a temporary recalibration. This helped me avoid shame and stay focused on the goal. I also tracked every expense, not to obsess, but to understand patterns. This data revealed hidden leaks — automatic renewals, unused memberships, duplicate services. Fixing these was painless but impactful. Cost reduction isn’t about deprivation — it’s about intentionality. When done wisely, it doesn’t shrink your future; it protects it.

Turning Assets Into Liquidity — Without Losing Everything

When cash runs low, selling assets becomes a tempting solution. But selling under pressure often means accepting low offers and losing long-term value. I faced this when I considered selling my home. It was my largest asset, and a quick sale could have covered my debts. But I knew that selling in a panic would mean accepting far below market value — and losing a stable place to live. Instead, I explored alternatives that provided liquidity without permanent loss.

The first step was valuation. I hired a professional appraiser to determine the true worth of my assets — home, vehicles, equipment, and investments. This gave me a clear baseline and prevented emotional decisions. I then prioritized assets based on liquidity, emotional attachment, and future utility. For example, my office equipment had low personal value but could generate cash through sale or lease. I chose to lease it to a startup for six months, earning steady income while retaining ownership.

For larger assets, I considered partial solutions. Instead of selling my home, I explored a home equity agreement — a structured arrangement where an investor provides cash in exchange for a share of future appreciation. This gave me immediate funds without a mortgage or monthly payments. I also sold a portion of my investment portfolio, focusing on underperforming assets with low tax implications. This minimized penalties and preserved growth potential in stronger holdings.

Timing was critical. I avoided fire sales by setting minimum price thresholds and waiting for offers that met them. I also used online marketplaces and industry networks to reach broader buyers, increasing competition and value. The goal wasn’t to liquidate everything, but to unlock enough cash to stabilize my situation. By treating asset conversion as a strategic process — not a desperate act — I preserved both capital and options. Liquidity doesn’t have to come at the cost of long-term security.

The Mindset Shift That Changes Everything

Rebuilding finances starts with rebuilding mindset. In the months after the crash, I battled shame, self-doubt, and the urge to hide. I felt like a failure, not just financially, but personally. I avoided calls from friends, skipped social events, and spent nights replaying every decision that led to the collapse. But I eventually realized that guilt doesn’t fix problems — clarity does. The turning point came when I reframed failure as feedback. Instead of asking, “Why did I fail?” I started asking, “What can I learn from this?”

This shift didn’t happen overnight. I began with small practices. Each morning, I wrote down three financial facts — not emotions, but objective truths: bank balance, upcoming bills, income sources. This grounded me in reality. I also started a decision journal, recording every financial choice and my reasoning behind it. Later, I reviewed these entries to spot patterns — when I acted impulsively, when I delayed necessary actions, when I let fear override logic.

I also established daily check-ins: 10 minutes each evening to review spending, assess progress, and plan the next day. This created rhythm and control. I stopped seeing money as a measure of worth and started seeing it as a tool — neutral, manageable, and responsive to disciplined action. I allowed myself to feel the stress without letting it dictate decisions. This emotional regulation was as important as any budget.

Another key was accepting that recovery is not linear. There were setbacks — unexpected bills, slow progress, moments of doubt. But I learned to measure progress by consistency, not perfection. Showing up every day, making small smart choices, staying aligned with my plan — that was success. The mindset shift didn’t erase the pain, but it transformed it into power. Financial resilience begins not in the bank account, but in the mind.

Rebuilding Smarter: Financial Planning That Actually Sticks

Today, my finances are stronger not because I avoided failure, but because I learned from it. The plan I follow now isn’t based on hope — it’s built on habits that survive real life. The first habit is regular stress-testing. Every quarter, I simulate a crisis: What if income stops? What if expenses double? I run the numbers and adjust my firewall accordingly. This keeps me prepared without living in fear.

The second habit is automation. I’ve set up automatic transfers to my firewall account, retirement fund, and investment portfolio. These happen the day after payday, before I can spend the money. This ensures consistency and removes willpower from the equation. I also use automated alerts for low balances, large transactions, and upcoming bills. These small systems create a safety net of discipline.

The third habit is early warning signs. I track key financial indicators — cash flow trends, debt-to-income ratio, savings rate — and set thresholds for action. If any metric crosses a red line, I trigger a review. This prevents small problems from becoming crises. I also schedule annual financial reviews with a trusted advisor, not to delegate responsibility, but to gain objective feedback.

Most importantly, I’ve embraced imperfection. A good financial plan isn’t one that never fails — it’s one that recovers quickly. It includes margin for error, room for adjustment, and compassion for human mistakes. I no longer tie my self-worth to my bank balance. Instead, I measure success by resilience — by how calmly I can respond when things go wrong.

Financial strength isn’t the absence of crisis. It’s the presence of preparation, the clarity of mindset, and the courage to rebuild. If you’ve ever feared losing it all, know this: you’re not alone, and you’re not helpless. With the right structure, the right habits, and the right perspective, you can survive — and emerge stronger than before.